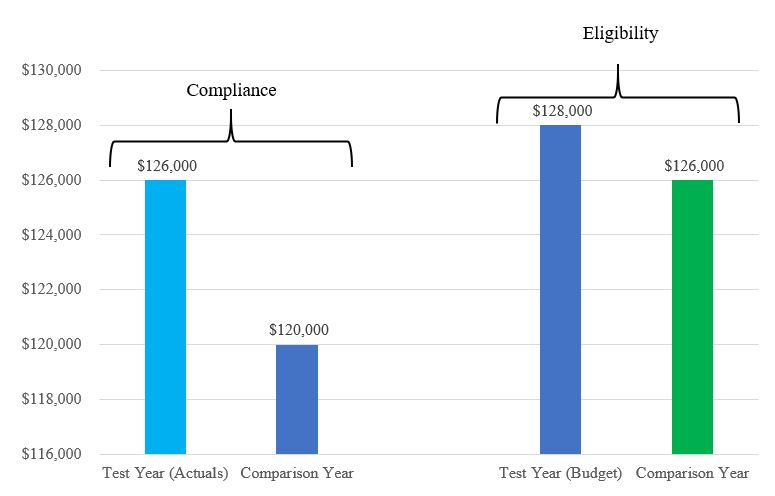

MOE Test Years

To meet the MOE requirement, the LEA must spend the same amount or more in the test year as it did in the comparison year. There are two years used when an LEA is preparing its year-end reports:

- The year that it is closing (the compliance standard)

- The new budget year (the eligibility standard)

For example, if the LEA is closing the 2025-26 fiscal year, the test years will be the following:

- The 2025-26 actual expenditures (for compliance)

- The 2026-27 budgeted expenditures (for eligibility)

This is a Federal requirement found in CFR 300.203(a) & 300.203(b). For LEAs that use the SACS web-based financial system, these two tests are found within two MOE reports: The SEMA and the SEMB.