WorkAbility Reporting

Member school districts that are participating in the Fresno County SELPA's WorkAbility grant must submit two fiscal reports: (1) a Mid-Year Report, which is due at the end of January, and (2) an End-of-Year Report, which is due at the end of May

Mid-Year Report

The WorkAbility Mid-Year Report is due January 31st of each year, and covers expenditures incurred or obligated between July 1 and December 31 of the fiscal year. Participating school districts will use the prescribed form to complete the report, and attach a budget report as evidence of the amount. Any amounts not supported by the budget report must be supported by other evidence.

End-of-Year Report

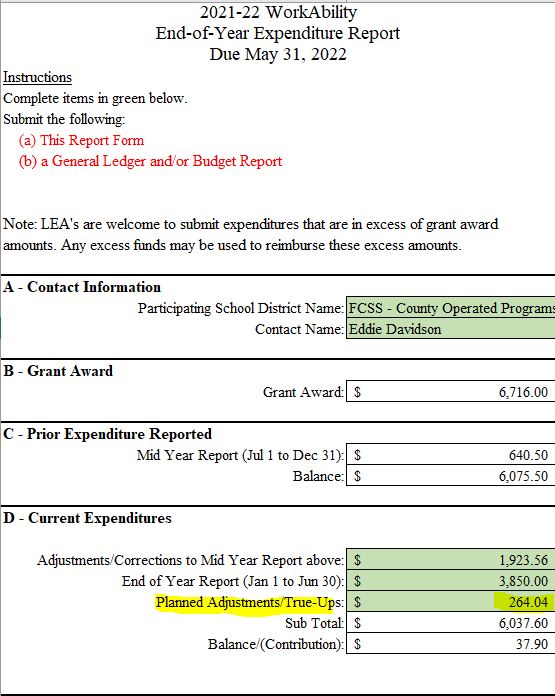

The WorkAbility End-of-Year Report is due May 31st of each year, and covers the following:

- Any adjustments or corrections to the mid-year report

- The end-of-year report that is substantiated by the member school district's general ledger report

- Any planned adjustments or true-ups

End-of-Year Planned Adjustments/True-Ups

Because the End-of-Year Report is due before the end the fiscal year, remember to include any legally obligated expenditures that have not yet been recorded in the school district's financial system. A list of legally obligated expenditures can be found here: CSAM Procedure 765 - Recognition of Legal Obligation in Reporting for Federal Grants

Additionally, be cognizant of your school district's pay periods for student wages. As students will likely submit a timesheet, the pay period may be much later. For example, if a student worker submits a timesheet for June on June 30th, the pay period may be July 30th. That July 30th payroll may likely be recognized in the General Ledger as an expenditure in the subsequent fiscal year.

Both the legally obligated expenditures and the student wages that are not yet recorded in the school district's general ledger may be included in the End-of-Year Report under the line "End-of-Year Planned Adjustments/True-Ups". Please provide documentation of the amount such as vendor quotes or student wage calculations.

Student Workers and Benefits

Student workers and the employer may not pay taxes such as Social Security, Medicare, and SUI if the student meets the definition of a "student worker". In short, a student may meet the definition when the student is attending classes and working in the LEA where the student attends school. In the summer months, however, if a student is not attending any classes while working at the LEA where the student attends, the student may be moved to the classified payroll. As a result, both the employee and employer pay Social Security, Medicare, and SUI. Confirm the status of your student worker with your LEA's payroll department.

Example

A student worked 18.50 hours in June. The student will submit a timesheet, but will not be paid until the end of July. The expenditure will not be reflected on the school district's general ledger for the year. The school district calculates the salary and wages at $264.04:

| Student Initials | ed |

| Student Hours Worked | 18.50 |

| Hourly Rate | $14.00 |

| Total Salary | $259.00 |

| Benefit Rate | 0.01938 |

| Employer-paid benefits | $5.02 |

| Total Salary and Benefits | $264.04 |

The school district may add $264.04 to its End-of-Year Report under the Planned Adjustments/True-Ups: